Cabinet Resolutions

Thailand’s accession to the Apostille Convention

The Cabinet passed a resolution approving Thailand’s accession to the Convention Abolishing the Requirement of Legalization for Foreign Public Documents (Hague Apostille Convention). Once fully implemented (approx. 6 months from the accession), public documents from Thailand will be legally recognized by member states by following a standardized simplified process without requiring the legalization through the consular. (*not yet completed the accession process)

https://treaties.mfa.go.th/th/content/การเข้าเป็นภาคีอนุสัญญา-apostille-ของประเทศไทย

Government Gazette

Small solar rooftop installations are to be exempted from requiring building alteration permits.

The installation of a solar rooftop project weighing below 20 kilograms per square meter will no longer require a building alteration permit, as it will not be considered a building alteration under the Building Control Act.

However, such an installation will still be subject to the permit/ license/ notification requirements under the Energy Industry Act.

https://ratchakitcha.soc.go.th/documents/94829.pdf

Tax incentives for solar rooftop installation and the purchase of energy-efficient equipment.

Solar rooftop installation: Individual taxpayers are entitled to tax exemption equal to the cost of equipment and installation of a solar rooftop system on a residential building connected to the grid of the Metropolitan Electricity Authority (MEA) or the Provincial Electricity Authority (PEA), up to a maximum of THB 200,000 (approx. EUR 5,400). The exemption applies to one system per taxpayer, to be claimed within the tax year where the system is successfully connected to the grid. These expenses cannot be used in conjunction with the benefits outlined in Point B below.

While obtaining permission to connect the solar rooftop to the grid is required, receiving payment for surplus electricity fed back into the grid is unlikely, as it is subject to additional requirements and is limited to a specified quota

B. Energy-efficient machinery and equipment: Individuals with incomes under Section 40 (5), (6), (7), (8) of the Revenue Code (such as: , asset lease, independent professions, contractor, entrepreneurs, etc.), companies, and juristic partnerships are entitled to deduct 50% of expenses/cost paid for investment in high-efficiency machinery, equipment, or materials certified with a 5-star energy-efficiency label of the Department of Alternative Energy Development and Efficiency (DEDE) and Electricity Generating Authority of Thailand (EGAT).

Further Conditions (apply to both points A. and B.)

- The expenses must be incurred at the latest by 31 December 2028;

- The expenses must be paid to a registered VAT operator and supported by an electronic tax invoice;

- These expenses cannot be used, in whole or in part, as other tax exemptions under the Revenue Code, or as an expense for a tax-exempted business under the Investment Promotion Act, National Competitiveness Enhancement Act, and Eastern Economic Corridor Act.

https://ratchakitcha.soc.go.th/documents/104277.pdf

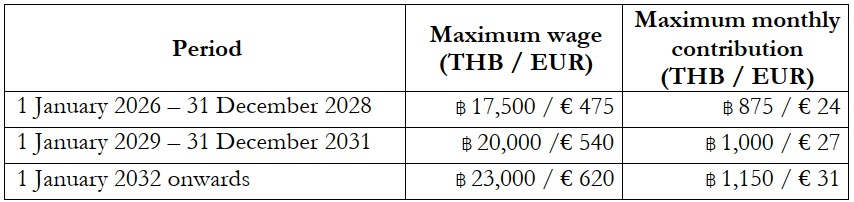

Increased wage ceiling under the Social Security Act

Under Section 33 of the Social Security Act, the monthly contributions for both employers and employees to the Social Security Office are based on 5% of the employees’ wage, with the maximum wage capped at THB 15,000 (approx. EUR 400), hence a maximum monthly contribution of THB 750 (approx. EUR 20). This wage ceiling had been applicable for the past 30 years until recently.

Now, the wage ceiling has been raised, which results in an increase in the maximum monthly contribution as follows:

(In comparison: the maximum total amount employer and employee together have to pay to the German social security system (covering health, accident and pension plan is EUR 3,020 or THB 110,000 or USD 3,500, so the maximum contribution to the social security system in Germany is over 100 times higher than in Thailand)

Such a wage ceiling increase will also lead to some increases of the employees’ benefits entitlement under Social Security, e.g., unemployment benefits (30%/ 60% wage), payment during maternity leave (50% wage), as they are also subject to the same wage ceiling.

https://ratchakitcha.soc.go.th/documents/98728.pdf

Amendment to the Penal Code re: Sexual Harassment

This amendment introduces “sexual harassment” as a distinct criminal offence, and adds protection for individuals regardless of their genders, ages, and identities. Key changes include:

- Sexual harassment: Sexual harassment is defined as any act, whether physical, verbal, by gesture, communication, watching, stalking, or through computer systems or electronic devices, that has a sexual connotation and is likely to cause the victim distress, embarrassment, humiliation, fear, or a sense of sexual insecurity.

- Expanded definition of rape: The definition is broadened to cover penetration using any body part or object and is made gender neutral.

- Online content takedown: Courts may order the removal of content which is considered sexual harassment from computer systems.

- Protective order for victims: Courts may issue protective orders prohibiting the defendant in a sexual harassment case from approaching or contacting the victim for a period not exceeding two years, regardless of whether the defendant is convicted.

https://ratchakitcha.soc.go.th/documents/94160.pdf

Tax deduction for the purchase of a Visual Arts art piece

The purchase of a “Visual Arts” art piece, e.g., painting, print, made during 1 January 2025 – 31 December 2027, is eligible for a personal income tax deduction for up to THB 100,000 (approx. EUR 2,700), subject to further conditions under the regulation.

https://ratchakitcha.soc.go.th/documents/94483.pdf

Increased expense deduction for artists

Fine-art artists (e.g., drawing, casting, sculpting) earning assessable income under Section 40(6) of the Revenue Code, as an independent profession, are now entitled to claim a fixed-rate expenses of 60% (increase from the original 30%), commencing from assessable income received in 2025 onward.