Welcome back to the first issue of our Legal/Tax News Update (Thailand) in 2016.

Tax Amnesty 2016 and SME Tax Reduction

As part of the government’s tax reforms, two new laws were announced in the Royal Gazette on 1 January 2016 and effective on the same day: 1) the Royal Act on the Exemption and Support for Tax Operation under the Revenue Code B.E. 2558 (also widely known as the “Tax Amnesty”) and 2) the Royal Decree under the Revenue Code on the Tax Rate Reduction and Exemption (No. 595) B.E. 2558 (“Royal Decree No. 595”).

Royal Act on the Exemption and Support for Tax Operation under the Revenue Code B.E. 2558 (a.k.a. Tax Amnesty)

The aim of the Tax Amnesty is to discharge Small and Medium-sized Enterprises (SMEs) for any past tax infringements. The Revenue Department (RD) also wishes to persuade SMEs to enter the formal tax system because only approximately 30% of SMEs are currently in the tax system. Moreover, the RD wants SMEs to maintain a single financial account principle (some Thai entities make 2 accounting books, 1 real book and 1 for tax filing).

The principle of this Tax Amnesty shall to allow the entities and the RD to move forward together, by waiving tax audits and penalties for previous fiscal years.

Eligible juristic persons: Only companies or juristic partnerships with revenue less than THB 500 million (approx. EUR 12.5 Mio) during the last full (12 months) fiscal year (ending on or before 31 December 2015) are eligible, except the following entities:

- Entities being investigated and having received a summon for tax audit before 1 January 2016;

- Entities being audited under Section 88/3 of the Revenue Code (site visit) before 1 January 2016;

- Entities who issued or used false tax invoices, or used false expenses;

- Entities being prosecuted by the police, the public prosecutor, or in court.

Section 5 of the Tax Amnesty further states that in case the eligible entity claims for any tax refund, the RD has the right to invetigate and audit the entity under the normal procedure of the Revenue Code.

Exemption Privileges: The eligible entities are exempted from any tax audit, tax inquiry, tax assessment or order to pay tax, and any criminal charges under the Revenue Code for:

- income derived in or before the fiscal year beginning before 1 January2016 (Corporate Income Tax, CIT); and

- value of tax base (Value Added Tax, VAT), gross receipts (Special Business Tax, SBT), and issuance of instrument (Stamp Duty) occurred before 1 January 2016.

- Registration and Conditions: To be eligible for the above privileges, the eligible entity has to:

- register with the RD until 15 March 2016;

- submit correct tax filing for CIT, VAT, SBT, and Stamp Duty, starting with the fiscal year commencing on or after 1 January 2016;

- produce correct financial accounts (to be in line with the truth), starting with the fiscal year commencing on or after 1 January 2016; and

- not conduct any acts of tax avoidance.

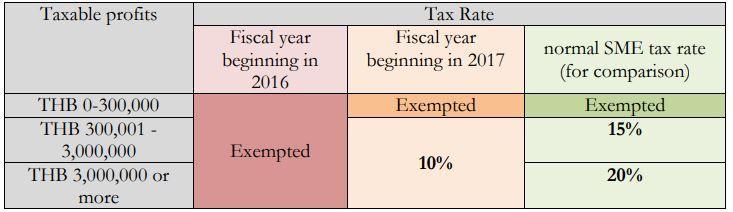

Royal Decree under the Revenue Code on the Tax Rate Reduction and Exemption (No. 595) B.E. 2558

- In addition, the government has enacted Royal Decree No. 595 for the exemption and reduction of corporate income tax for SMEs.Eligible SMEs: The SMEs have to fulfil the following three conditions to be eligible for the special tax rate:having less than THB 5 million (approx. EUR 125,000) registered capital and less than THB 30 million (approx. EUR 750,000) income from sales and services (normal SME condition);

being registered as operator under the abovementioned Tax Amnesty scheme; and the right under the Tax Amnesty law is not revoked (i.e. the entity has to continuously fulfil the conditions of the Tax Amnesty scheme).

Tax Rate: The reduced tax rates are as follows:

Business Collateral Act B.E. 2558 (2015)

On 5 November 2015, the Business Collateral Act B.E. 2558 (2015) (“BCA”) has been announced in the Royal Gazette. The law will come into effect 240 days thereafter, i.e. on 2 July 2016.

Principle: In order to strengthen the Thai economy, the government is trying to support small and medium-sized enterprises (SMEs). One of the greatest obstacles for SMEs is to apply for a loan or credit line with banks due to the lack of collateral to secure the loan.

Currently, asset collateral can be used to secure a debt in the following common ways:

Mortgage: This is the most common way to secure debts, but mortgage is only available for certain types of assets under the law (e.g. land, buildings, machinery, etc.).

Pledge: For other assets, the debtor can pledge such assets to secure a loan. The biggest disadvantage of pledging is that the pledged assets have to be physically handed over to the creditor. If the pledged assets are returned to the debtor, the pledge is considered to be revoked. As a consequence, the debtor cannot use these assets during the time they are pledged to the creditor.

To provide better access to finance via loans, the BCA intends to give debtors more options to secure their debt, and thereby increasing the chance to get a loan and obtaining the financial means needed to operate their business.

Parties involved: Under Section 6 of the BCA, the person who provides collateral (“Collateral Provider”) can be an individual or a juristic person. However, the person who can receive business collateral (“Collateral Receiver”) has to be a financial institute (or another person prescribed by Ministerial Regulation).

Business Collateral Agreement and Registration: Section 13 of the BCA requires a written Business Collateral Agreement (“Agreement”). The Agreement (as well as its amendments and cancellations) has to be registered at the Business Collateral Registration Office (“BCRO”), Department of Business Development.

Business Collateral: The assets, specified in Section 8 of the BCA, that can be registered as business collaterals are:

Business, defined in Section 3 of the BCA as “…assets used in the business of the Collateral Provider and other rights related to the business…”;

Claim, defined in Section 3 of the BCA as “…claims for payments or other claims, but not include claim under instrument” (e.g. bill of exchange, etc.);

movable properties used in the security provider’s business (e.g. machinery, inventory, or raw materials);

immovable property (in case, the security provider is operating in the real estate business);

intellectual property; or

any other asset as stipulated in Ministerial Regulations issued under the BCA;

Legal Effect of the Agreement: The Agreement’s legal consequences are similar to those of a mortgage agreement. For example, the Collateral Receiver has a preferential claim over the collateral, and the collateral right will not perish even if the asset is transferred to a third party. The Collateral Receiver will also become a secured debtor of the collateral under the Bankruptcy Act. Collateral Enforcement: The execution into business collaterals can be separated into the following two categories:

– Enforcement of the Businesses: In case of Businesses as collateral, the execution has to be performed by a licensed “Collateral Enforcer”, who will determine the suitable way to sell the Business and distribute the sales price. These Collateral Enforcers have to be registered with the BCRO;

– Enforcement of other assets: These assets can be either 1) sold or disposed for sales price distribution, or 2) executed by the way of collateral foreclosure (similar to mortgage). For such executions, a licensed Collateral Enforcer is not required.

Penalties: The BCA specifies several criminal penalties, both on the Collateral Provider and the Collateral Receiver (e.g. for withholding the truth or providing falsified statements, unlawfully taking the collateral, using or divulging confidential information, etc.), as well as on the Collateral Enforcer for corruption offenses.

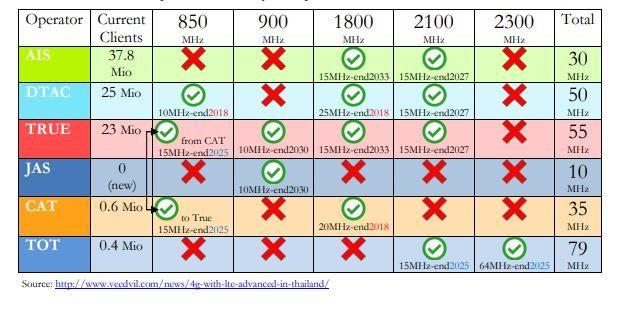

4G Auctions (Battle for Spectrum)

In December 2015, the National Broadcasting and Telecommunication Commission (NBTC) conducted a 900 MHz spectrum auction for highly competitive mobile services. It was the fight among AIS, Dtac, True Move (the big 3 operators) and Jasmine Mobile (a new player in the mobile service market, currently operating in broadband internet).

After almost 5 days and almost 200 rounds of auction, True Move and Jasmine emerged as the winners, receiving 10MHz each in the 900 MHz spectrum. These licenses will be valid for 15 years.

Winning bid: The final bid price was THB 76.26 billion (approx. EUR 1.9 billion) for True Move and THB 75.65 billion (approx. EUR 1.89 billion) for Jasmine. The auction prices are relatively high compared to the 900 MHz spectrum of other countries, ranking 3rd place in world in term of auction price per capita:

– 1st Hong Kong: THB 122.6/1MHz/capita (approx. EUR 3.065);

– 2nd Hungary: THB 73.4/1MHz/capita (approx. EUR 1.835);

– 2nd Hungary: THB 73.4/1MHz/capita (approx. EUR 1.835);

1800 MHz auction: The final bid price in the 900 MHz auction was almost twice the price in the previous 1800 MHz auction which was held one month earlier. In the 1800 MHz auction (2 slots), True Move won the license for 15 MHz (15 years) at the bidding price of THB 39.79 billion (approx. EUR 0.94 billion), while AIS also won the same at THB 40.98 billion bidding (approx. EUR 1.24 billion). However, the 900 MHz spectrum provides more coverage in terms of area.

Next auctions: The NBTC expects to further auction the 800 MHz spectrum in 2018 and 700 MHz spectrum in 2023. After the concession agreement with TOT ends in 2025, the NBTC aims to auction off the 2300 MHz spectrum as well.

Current situation: After the auction in December 2015, the current spectrums used by the operators in Thailand are as follows:

Establishment of Special Jurisdiction Court of Appeal

We reported in the previous issue of our Legal & Tax News Update (NU004) that the Supreme Court is trying to speed up the case proceedings by limiting the cases which can be appealed to the Supreme Court (Amendment No. 27 of the Civil Procedure Code).

Following the aforementioned amendment, the Supreme Court will further reduce the tasks at hand by enacting several laws related to the establishment of the Special Jurisdiction Court of Appeal (SJCA) to harmonise the appeal system in Thailand for special jurisdiction cases.

These laws were announced on 14 December 2015 and became effective the following day.

Special Jurisdiction Cases: Special Jurisdiction Cases (SJCs) under Section 3 of the Establishment of the SJCA Act B.E. 2558 are the following cases:

– Intellectual Property and International Trade cases;

– Taxation cases;

– Labour cases;

– Bankruptcy cases;

– Juvenile and Family cases;

Prior to the establishment of the SJCA and the subsequent amendment of related laws, these types of cases are appealed from the Court of First Instance having jurisdiction over the case (i.e. Intellectual Property and International Trade Court, Taxation Court, Labour Court, Bankruptcy Court, and Juvenile and Family Court) directly to

the Supreme Court. However, as the Supreme Court limited the right to appeal normal civil cases to the Supreme Court, the appeal system for SJCs had to be syncronised as well.

The SJCA is initially planed to be established next to the old Supreme Court (close to Sanamluang) but is not yet operational. Until the official opening of the SJCA, the SJCs will be appealed to the Supreme Court as usual.