Although Lorenz & Partners always pays great attention on updating information provided in newsletters and brochures we cannot take responsibility for the completeness, correctness or quality of the information provided. None of the information contained in this newsletter is meant to replace a personal consultation with a qualified lawyer. Liability claims, regarding damage caused by the use or disuse of any information provided, including any kind of information which is incomplete or incorrect, will therefore be rejected, if not generated deliberately or grossly negligent

I. Introduction

In the context of international trade, importers are exposed to a heightened risk of non-performance by the exporter in terms of their contractual obligations. Besides the commercial risks of insolvency the exporter, may become incapable of performing its duties due to the risks attached to selling to public or private entities in territories where political factors may have an impact. Some of these political risks include the cancellation of import or export licences, the imposition of embargos, and the frustration of contracts due to war or confiscation.

Importers in international trade therefore often wish to have a security that the exporter will fulfil its obligations. To secure the contract, an exporter may be required to provide a guarantee that takes the form of a Demand Guarantee. Demand Guarantees provide protection to the importer against late, defective or non-performance by the exporter or contractor. Many contractors must issue guarantees in the form of tender guarantees (also “bid guarantees”), advance payment or stage payment guarantees, performance guarantees and retention bonds.

Demand Guarantees must be differentiated from another financial instrument used in international trade, the Letter of Credit (“L/C”). L/Cs provide security for the exporter against non-payment.[1] The typical Demand Guarantee, however, is issued to reduce the risk of non-performance.

[1] For more information on L/Cs and other instruments to secure performance and obligations under contracts, please refer to our Nerwsletter No. 13.

II. Legal Nature and Features of Demand Guarantees

A Demand Guarantee is a contract by which a guarantor, typically a bank or another financing institution, undertakes to pay to the importer/employer/contactor a sum of money (usually up to a maximum amount) upon representation of a demand together with any documents specified under the terms of the bank’s guarantee.

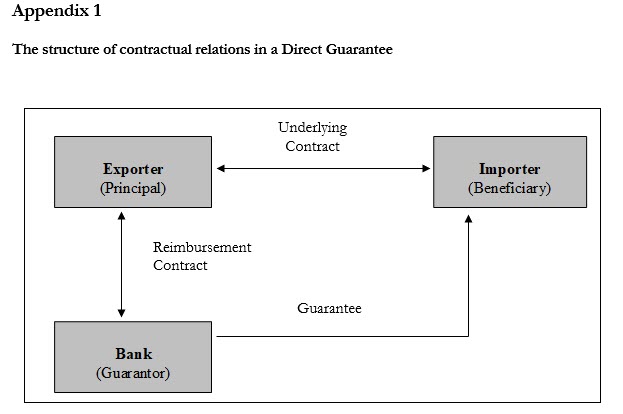

1. The Contractual Relations: Direct and Indirect Guarantees

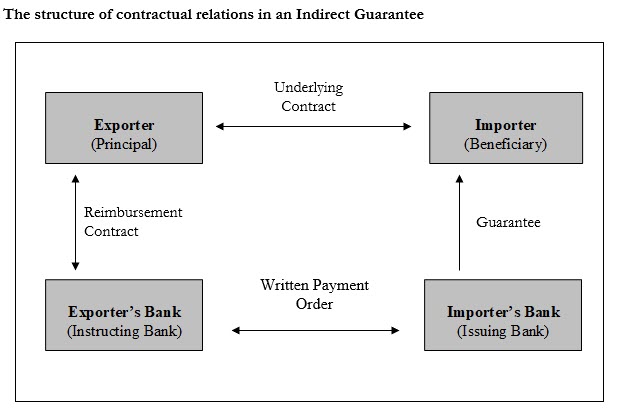

A Demand Guarantee can be issued as a Direct or Indirect Guarantee. Whereas in the constellation of a direct guarantee three subjects are involved, there are four subjects engaged in an Indirect Guarantee.

A Direct Guarantee is provided by the exporter’s bank to the importer/employer (beneficiary) directly. In this case there are three contracts:

- the underlying contract between the exporter/contractor and the importer/employer (e.g. a sales contract, (plant) construction contract or a contract for services);

- the reimbursement contract between the exporter/contractor and its bank; and

- the actual Demand Guarantee between the bank and the importer/employer.

The structure of the contractual relations in a Direct Guarantee can be seen in Appendix 1 below.

In case of an Indirect Guarantee, the guarantee is provided by the importer’s bank.

The exporter’s bank (instructing bank) instructs the importer’s bank (issuing bank) to issue the guarantee in favour of the beneficiary. It is the issuing bank only that assumes the obligations of the guarantor. It does not act as an agent of the instructing bank. In this case, there are four contracts. There neither is a contractual relationship between the beneficiary and the instructing bank nor between the exporter and the issuing bank.

The structure of the contractual relations in an Indirect Guarantee can be seen in Appendix 1 below.

2. Legislation Governing Demand Guarantees

The characteristics of a Demand Guarantee depend on the applicable law and jurisdiction. In general, a bank guarantee will contain a provision stating the choice of law. In absence of such provision, the conflict of law provisions will most often provide that the location of the bank’s office will be the decisive criterion regarding the applicable law, since the bank renders the characteristic main service (Art. 34 (a) Uniform Rules for Demand Guarantees; “URDG”).

In addition to the national law, the International Chamber of Commerce (“ICC”) has published several sets of example rules concerning Demand Guarantees: The “Uniform Rules for Contract Guarantees” of 1978 (Publication No. 325) did not gain wide acceptance. In 1992, the “Uniform Rules for Demand Guarantees” were issued, and in 2010 a revised version of the URDG (Publication No. 758) was released.

The ICC’s URDG reflect international standard practice in the use of demand guarantees and balance the legitimate interests of all parties. More than an update of the existing rules, the revised URDG 758 is a new set of rules for the 21st century that has been in effect since the 01 July 2010. Although not used frequently, it is recommended to incorporate them in international contracts since these rules state the most common and widely used practice in international trade.

Under German law and the URDG (Art. 5 (a) URDG), the main feature of a Demand Guarantee is that it is legally independent from the underlying contract between the exporter/contractor and the importer/employer, i.e. it is an abstract payment undertaking. In general, payment must be made upon calling of the guarantee, e.g. upon presentation of a written demand that complies with the provisions of the Demand Guarantee. Many Demand Guarantees are payable on first demand without any additional documents (so-called First Demand Guarantees). This reflects their origin in replacing cash deposits. However, First Demand Guarantees are increasingly requiring a statement indicating that the exporter/contractor is in breach of the underlying contract, despite this being contradictory to their nature of being payable on first demand.

III. Special Risks of Demand Guarantees: Unfair Calling and Expiration

There are two major risks: Unfair calling of the guarantee and the absence of an expiration date of the guarantee.

1. Unfair Calling

Since the Demand Guarantee is legally separate from the underlying contract, it contains the risk of being called for unfairly although the underlying contract’s conditions have been fulfilled. The URDG does not contain provisions regarding this case. Therefore, it depends on the jurisprudence and the legislation of the applicable national law to determine in which case a payment request is regarded to be unfair, giving the exporter/contractor a chance to prevent the bank from paying out the guaranteed sum.

Under German (procedural) law, the exporter/contractor may seek a “provisional injunction” (Einstweilige Verfügung) against the bank. However, the injunction will only be issued in case the beneficiary obviously misuses its position. In other jurisdictions, there are no legal remedies at hand to prevent unfair calling of Demand Guarantees. Apart from that, experience shows that legal actions prior to calling are frequently not successful.

2. Expiration

A clear expiry date should be stated in the Demand Guarantee. The URDG contain a set of expiry provisions. A standard clause is: “This guarantee shall expire, even if this document is not returned, on … at the latest.” However, some countries, especially in the Middle East, may not accept a Demand Guarantee which includes an expiry date as this may not be enforceable under local laws. Further, cases are known where exporters/contractors were pushed to extend the expiration date by threatening to call the Demand Guarantee

IV. Insurance

The risk of unfair calling (as well as of fair calling, e.g. where the contract would not be performed for political reasons, such as non-renewal of export licences) may be insured. The insurers range from national export credit agencies to private insurers. Although unfair calling of a guarantee does not occur often, in certain cases it may be recommendable to seek insurance coverage.

V. Summary

Special prudence should be exerted when drafting the Demand Guarantee. Critical circumstances are the expiration of the guarantee, the choice of law and its legal separation from the underlying contract. Especially when doing business in regions where the performance of a contract depends on political impact; it might be recommendable to take out an unfair calling insurance.